Nonprofit Functional Expense Classification & Reporting Requirements

A well-designed, rational expense allocation process is an absolute necessity for every Nonprofit (NFP), as stakeholders want to know and have a right to know, how the organization uses its resources to accomplish its mission.

This article provides an overview of the financial reporting requirements under generally accepted, accounting principles (GAAP), including the provisions of the Financial Accounting Standards Board(FASB) Accounting Standards Update (ASU) 2016-14, Presentation of Financial Statements of Not-for-Profit Entities.

Under ASU 2016-14, every NFP is now required to present its expenses by both nature and function, as well as a description of the methods used to allocate costs among program and support functions. NFPs shall report this information in one location- on the face of the statement of activities, as a schedule in the notes to the financial statements, or in a separate financial statement.

Functional Expense Classification

When determining the best approach to classify expense transactions, it’s important to have clarity on the meaning of program services and supporting activities under the standards. The FASB ASC provides the following definitions:

Functional expense classification - a method of grouping expenses according to the purpose for which costs are incurred. The primary functional classifications for NFPs are program services and supporting activities.

Program services - the activities that result in goods and services being distributed to beneficiaries, customers or members, that fulfill the purposes or mission for which the NFP exists. Those services are the major purpose for and the major output of the NFP, and often relate to several major programs.

Supporting activities - all activities of a NFP other than program services. They typically include (a) Management and general activities (b) Fundraising activities (c) Membership development activities.

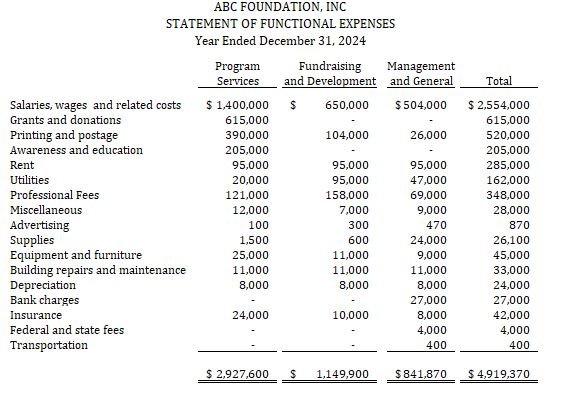

Sample Statement of Functional Expenses

Program Services

In order to accurately tell their story, most NFPs will report several program service categories. They have latitude in defining their major programs so that information provided is meaningful in understanding the expenses of the NFP’s service efforts. Factors to consider in determining the programs to present include the following:

Program objectives

Nature of services

Constituents served

Magnitude of the program to the NFPs overall activities

Budgetary categories

Oversight, regulatory, grant or other compliance requirements that separate the program from others

Other factors that may be relevant to the financial statement users

Supporting Activities

Supporting activities include management & general activities, fundraising activities and membership development activities. The specific definition of each activity is as follows:

Management & General Activities

Per the FASB ASC glossary, these are supporting activities that are not directly identifiable with one or more program, fundraising, or membership-development activities. They include:

Oversight

Business management

general record keeping & payroll

Budgeting

Financing, including unallocated interest costs

Soliciting funds other than contributions and membership dues. For eg. promoting the sale of goods or services to customers.

Administering government, foundation, and similar customer-sponsored contracts. For eg. billing and collection fees and grant and contract financial reporting

Making announcements concerning appointments

Producing and disseminating the annual report

Employee benefits management and oversight

All other management and administration except for direct conduct of program services, fundraising activities, or membership development activities

FASB ASC 958-720-45 clarifies that when those who usually are responsible for providing oversight and management spend a portion of their time directly conducting or supervising program services or categories of other supporting services, their salaries and expenses should be allocated among those functions.

Fundraising Activities

As defined in the FASB ASC glossary, fundraising activities are activities undertaken to induce potential donors to contribute money, securities, services, materials, facilities, other assets or time. A solicitation activity is considered fundraising regardless of whether the intended donor responded favorably to the solicitation or not. These activities include:

Publicizing and conducting fundraising campaigns

Maintaining donor mailing lists

Conducting special fundraising events

Preparing and distributing fundraising manuals, instructions and other materials

Conducting other activities involved with soliciting contributions from individuals, foundations government agencies, and others

Membership Development Activities

In the FASB ASC glossary, membership development activities include soliciting for prospective members and membership dues, membership relations, and similar and similar activities.'

If no significant benefits are provided to members in exchange for their payment, the substance of the membership development activities is considered fundraising for the purpose of functional expense reporting.

Other Supporting Activities

Although less common than the other three previously discussed supporting activities, some NFPs may have one or more of the following additional supporting activities:

Cost of sales activities that are not program activities. For example, a thrift shop operated to generate funding. The operating costs of such a thrift shop would be reported as a separate supporting activity.

A NFP may own an investment property that is rented to generate income. The expenses of owning and maintaining the property, and the costs of conducting the rental activities could be reported as a separate supporting activity.

Accounting for Expenses by Function

Direct Identification

Direct identification of specific expenses, which is also referred to as assigning expenses, is the preferable method of charging expenses to various functions. If an expense can be specifically identified with a program or supporting service, it should be assigned to that function. For eg. travel costs incurred in connection with a program activity would be assigned to that program.

Cost Allocation

Many expenses relate to more than one program or supporting activity, and direct identification is impossible or impractical, an allocation is appropriate. The cost allocation methodologies used should be rational and systematic, resulting in an allocation of costs that is reasonable. The allocation methodologies should be applied consistently over reporting periods given similar facts and circumstances.

There is no one-size-fits-all allocation model. Objective methods of allocating expenses are preferable to subjective methods. Allocations may be based on related financial or nonfinancial data. The guidance found in Title 2 U.S. Code of Federal Regulations(CFR) Part 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (Uniform Guidance), provides useful information on allocating costs.

Specific guidance to consider when allocating costs includes:

FASB ASC 958 provides general guidance to be used in the classification and allocation of fundraising costs.

FASB ASC 958-720-45-25 states that expenses associated with occupying and maintaining a building, such as depreciation, utilities, maintenance, and insurance may be allocated among a NFP’s functions based on the square footage of space occupied by each program and supporting service. If floor plans are not available, an estimate of the relative portion of the building occupied by each function may be made.

FASB ASC 958-720-45-24 states that interest costs, including interest on a building’s mortgage, should be allocated to specific programs or supporting activities to the extent possible. Interest costs that cannot be allocated should be reported as part of the management and general function.

Q&A section 6960.12, “Allocation of Overhead” (AICPA, Technical Questions & Answers), states that allocation of overhead is an inter-program transaction that should not be reported as revenue of the program providing the service, but rather as a reduction of expense for such program.

The Watch-Dog Agencies that rate the effectiveness of NFPs factor in the percentage of expenses devoted to programs, as a key component in the formulas they use to rate, monitor and compare NFPs. Donors and the press therefore, also track these percentages carefully. The “65/35 rule” is generally considered a good benchmark for NFP expense allocation. Generally, this means that at least 65% of total expenses should be allocated to program activities, and no more than 35% should be spent on supporting activities. This is however just a guideline, not a legal requirement. The exact breakdown will vary depending on the specific NFP and its operations.

We are here to assist with your NFP functional expense allocation. Please feel free to schedule a complimentary consultation below.