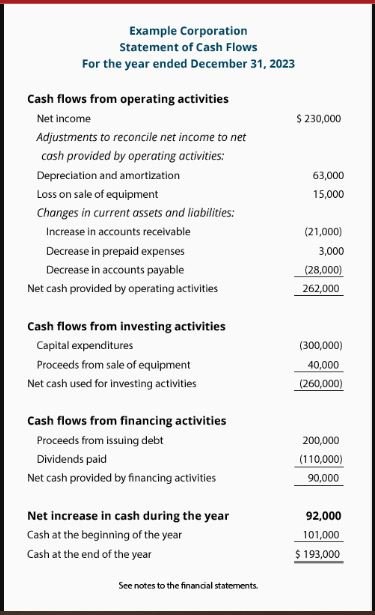

Sample Statement of Cash Flows

The primary objective of the statement of cashflows is to provide relevant information about the cash receipts and payments of an entity during the same period of time as the income statement. The statement reports cash flows in three categories, namely operating activities cash flows, investing activities cash flows and financing activities cash flows. The statement of cash flows may present operating cash flows either indirectly or directly. Preparers have consistently endorsed the use of the indirect method, primarily because the data is readily available from the other financial statements.

Operating Activities Cash Flows

These include all transactions that are not defined as investing or financing activities.

Cash inflows from operating activities include cash receipts from:

Sale of goods and services

Returns on loans, debt instruments and equity securities (for eg. interest & dividends)

Settlement of lawsuits

Cash refunds from vendors

Cash outflows from operating activities include cash payments to:

Vendors for goods and services

The government for taxes and duties

Lenders and other creditors for interest

Settle lawsuits and to make cash refunds to customers.

Investing Activities Cash Flows

Cash inflows from investing activities include the following:

Receipts from collections or sales of loans made by an entity

Receipts from sales of equity instruments of other entities

Receipts from sales of property, plant and equipment and other productive assets

Receipts from the sale of loans that were not specifically acquired for resale

Cash outflows from investing activities include the following:

Disbursement for loans made by the entity, and payments to acquire debt instruments of other entities

Payments to acquire equity instruments of other entities

Payments to acquire property, plant and equipment and other productive assets.

Payments to acquire a new business

Financing Activities Cash Flows

These include obtaining resources from owners and providing them with a return on their investment; restricted resources from donors stipulated for long term purposes , borrowing money and repaying amounts borrowed. More specific cash inflows and outflows include the following:

Cash inflows from financing activities include the following:

Proceeds from issuing equity instruments

Proceeds from issuing bonds, mortgages and other short or long term borrowing

Receipts for donor-restricted endowment fund

Cash outflows from financing activities include the following:

Payments of dividends or other distributions to owners of entities

Repayments of amounts borrowed

Payments for debt issue costs

Benefits of the Statement of Cash Flows

The information provided in a statement of cashflows, if used with related disclosures and information in the other financial statements, should help business owners/ leaders, investors, creditors and others (including donors) to do all of the following:

Assess an entity’s ability to generate positive net cash flows in the future

Assess an entity’s ability to meet its obligations and pay dividends

Assess an entity’s need for external financing

Assess whether an entity is generating a net positive cashflow from operations

Cash is king in any organization. An organization that is unable to generate net positive cashflows on a consistent basis is destined for failure. In light of this, the Statement of Cash Flows is an integral part of a full set of financial statements, and should be closely reviewed and analyzed as part of the assessment of any organization’s financial health.